Prepare to navigate the complexities of Brazilian tax filing with our in-depth guide to Tabelas IRS 2024. This comprehensive resource unravels the intricacies of tax deductions, credits, and brackets, empowering you to optimize your tax strategy and minimize your tax liability.

From understanding the standard deduction to exploring the nuances of itemized deductions, this guide provides a clear and concise roadmap to help you navigate the Brazilian tax landscape. Stay informed about the latest tax laws and regulations, ensuring compliance and maximizing your tax savings.

Introduction to Tabelas IRS 2024

The Tabelas IRS 2024, published by the Portuguese Tax and Customs Authority, provide crucial information for individuals and businesses to accurately calculate their tax obligations for the 2024 tax year. These tables include essential data such as tax brackets, standard deductions, and tax rates, ensuring compliance with the latest tax regulations.

The Tabelas IRS 2024 incorporate key changes and updates from previous years, reflecting adjustments made to the tax code and economic conditions. Understanding these changes is vital to avoid potential errors or overpayments during tax filing.

Types of Tabelas IRS 2024

- Tabela de Retenção na Fonte de IRS: Used to determine the amount of income tax withheld from salaries, pensions, and other forms of employment income.

- Tabela de IRS: Provides tax rates and brackets for calculating income tax liability based on taxable income.

- Tabela de Coeficientes de Encargos: Used to calculate deductible expenses for self-employed individuals and professionals.

Income Tax Rates and Brackets

The Portuguese Income Tax Code (Código do Imposto sobre o Rendimento das Pessoas Singulares – CIRS) establishes the income tax rates and brackets applicable to individuals for the year 2024. The tax rates vary according to the level of taxable income, which is determined by subtracting allowable deductions and exemptions from gross income.

Income Tax Brackets

The income tax brackets for 2024 are as follows:

- 0% on income up to €7,112

- 14.5% on income between €7,113 and €10,732

- 23% on income between €10,733 and €20,322

- 28% on income between €20,323 and €25,075

- 35% on income between €25,076 and €36,967

- 37% on income between €36,968 and €80,640

- 45% on income between €80,641 and €100,759

- 48% on income over €100,760

The tax liability is calculated by applying the applicable tax rate to the taxable income within each bracket. For example, an individual with a taxable income of €15,000 would pay 14.5% on the first €10,732 of taxable income and 23% on the remaining €4,268, resulting in a total tax liability of €2,303.04.

– Provide examples of eligible expenses for each type of deduction.

Eligible expenses vary depending on the type of deduction. Some common examples include:

- Business expenses: Costs incurred in the course of running a business, such as travel, meals, and office supplies.

- Medical expenses: Costs incurred for medical care, such as doctor’s visits, prescription drugs, and hospital stays.

- Charitable contributions: Donations made to qualified charitable organizations.

- Mortgage interest: Interest paid on a mortgage for a primary residence.

- State and local taxes: State and local income taxes, sales taxes, and property taxes.

Tax Credits

Tax credits are a valuable tool that can help you reduce your tax liability. Unlike deductions, which reduce your taxable income, tax credits directly reduce the amount of tax you owe. This means that tax credits can provide a more immediate and significant benefit than deductions.

There are a variety of tax credits available for individuals and families, including the following:

Earned Income Tax Credit (EITC)

The EITC is a refundable tax credit for low- and moderate-income working individuals and families. The amount of the credit you can claim depends on your income, filing status, and the number of qualifying children you have.

Child Tax Credit (CTC)

The CTC is a tax credit for parents of children under the age of 17. The amount of the credit you can claim is $2,000 per eligible child.

American Opportunity Tax Credit (AOTC), Tabelas IRS 2024

The AOTC is a tax credit for qualified education expenses paid for the first four years of post-secondary education. The maximum amount of the credit is $2,500 per eligible student.

Lifetime Learning Credit (LLC)

The LLC is a tax credit for qualified education expenses paid for undergraduate, graduate, or professional degree courses. The maximum amount of the credit is $2,000 per eligible taxpayer.

Retirement Savings Contributions Credit (Saver’s Credit)

The Saver’s Credit is a tax credit for low- and moderate-income taxpayers who make contributions to a retirement savings account, such as an IRA or 401(k). The maximum amount of the credit is $1,000 per eligible taxpayer.

To claim a tax credit, you must meet the eligibility requirements for the credit and complete the appropriate tax form. You can find more information about tax credits on the IRS website.

Taxable Income

Taxable income is the portion of your total income that is subject to taxation. It is calculated by subtracting certain deductions and exemptions from your gross income. Gross income includes all income from all sources, including wages, salaries, investments, and business income.

Sources of Income

Various sources of income are subject to taxation, including:

- Wages and salaries

- Tips and bonuses

- Investment income (dividends, interest, capital gains)

- Business income

- Rental income

- Royalties

- Annuities

- Pensions

- Lottery winnings

Deductions and Exemptions

Deductions and exemptions are subtracted from gross income to arrive at taxable income.

- Deductions reduce your taxable income dollar-for-dollar. Examples include:

- Mortgage interest

- State and local taxes

- Charitable contributions

- Exemptions are subtracted from your taxable income before applying the tax rates. Examples include:

- Personal exemption

- Dependent exemption

Marginal Tax Rates

Taxable income is taxed at different rates depending on your filing status and income level. These rates are known as marginal tax rates. The marginal tax rate is the rate that applies to the last dollar of taxable income.

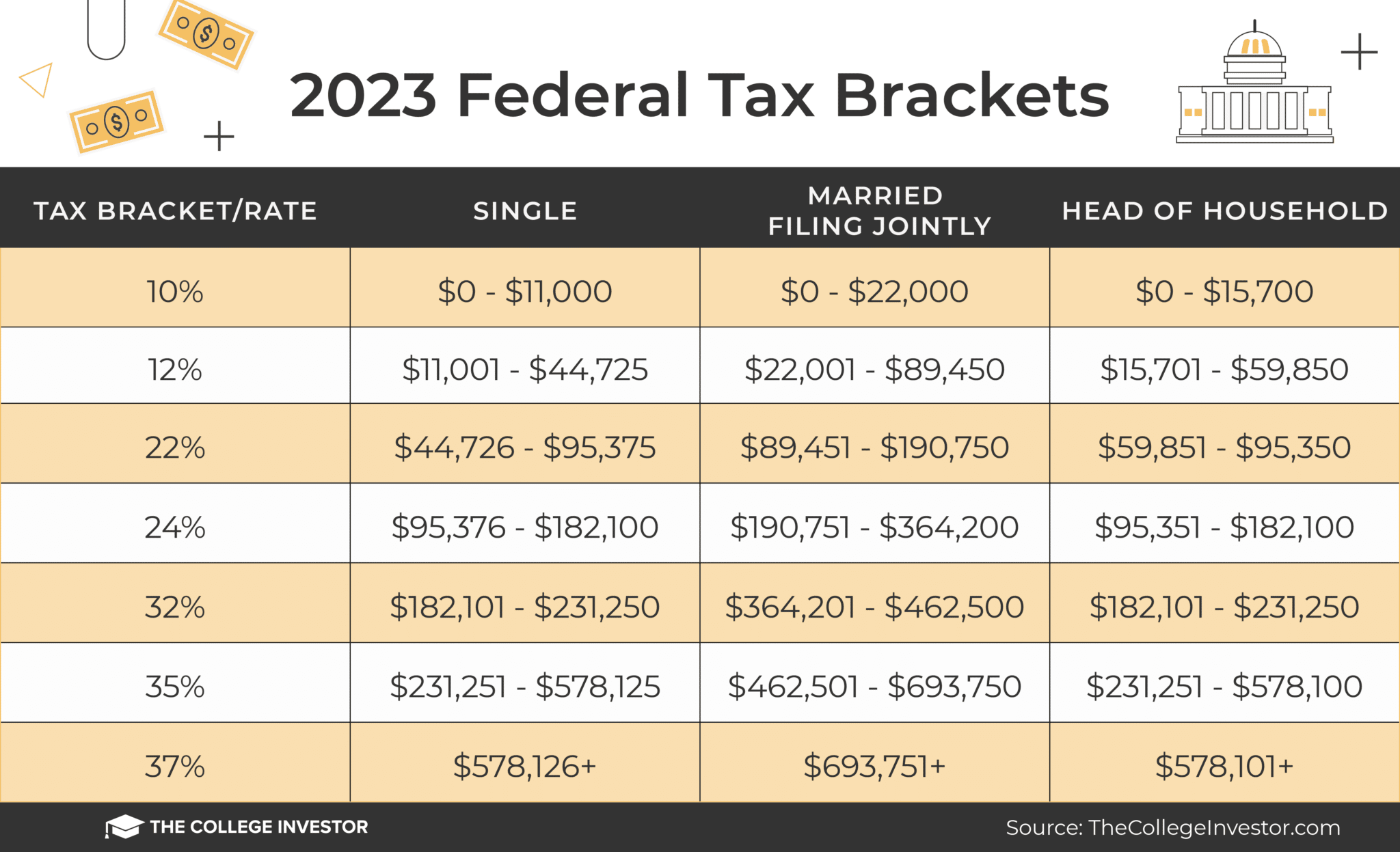

Tax Brackets

Tax brackets are ranges of taxable income that are taxed at different rates. The tax brackets for 2023 are as follows:

| Filing Status | Taxable Income | Tax Rate |

|—|—|—|

| Single | $0-$10,275 | 10% |

| Single | $10,275-$41,775 | 12% |

| Single | $41,775-$89,075 | 22% |

| Single | $89,075-$170,500 | 24% |

| Single | $170,500-$215,950 | 32% |

| Single | $215,950-$539,900 | 35% |

| Single | $539,900+ | 37% |

Tax Implications of Different Types of Income

Different types of income are taxed differently. For example, wages and salaries are taxed at ordinary income tax rates, while investment income is taxed at capital gains rates. Business income is taxed at the individual’s marginal tax rate.

Gross Income vs. Taxable Income

Gross income is all income from all sources. Taxable income is gross income minus deductions and exemptions.

Glossary

- Deduction: An expense that reduces taxable income.

- Exemption: A specific amount of income that is not subject to taxation.

- Gross income: All income from all sources.

- Marginal tax rate: The tax rate that applies to the last dollar of taxable income.

- Taxable income: The portion of your total income that is subject to taxation.

- Tax bracket: A range of taxable income that is taxed at a specific rate.

Tax Forms and Deadlines

The Internal Revenue Service (IRS) requires individuals and businesses to file specific tax forms by established deadlines. These forms serve as a means of reporting income, deductions, and tax liability. Understanding the required tax forms and adhering to the filing deadlines is crucial to avoid penalties and ensure compliance with tax laws.

Required Tax Forms for 2024

The primary tax form for individuals is Form 1040, which is used to report income, calculate tax liability, and claim deductions and credits. Depending on individual circumstances, additional schedules may be required to accompany Form 1040, such as:

– Schedule A (Itemized Deductions)

– Schedule B (Interest and Ordinary Dividends)

– Schedule C (Profit or Loss from Business)

– Schedule D (Capital Gains and Losses)

– Schedule E (Supplemental Income and Loss)

For businesses, the specific tax forms required vary based on the type of business entity. Some common forms include:

– Form 1120 (Corporate Income Tax Return)

– Form 1065 (Partnership Return of Income)

– Form 1041 (U.S. Income Tax Return for Estates and Trusts)

Filing Deadlines and Penalties for Late Filing

The general filing deadline for individual tax returns is April 15th. However, if April 15th falls on a weekend or holiday, the deadline is extended to the next business day. For 2024, the filing deadline for individual tax returns is Tuesday, April 16th.

For businesses, the filing deadlines vary depending on the type of entity. For example, corporations generally have an April 15th deadline, while partnerships and trusts have an extended deadline of March 15th.

Penalties for late filing can be significant, so it is important to file tax returns on time. The IRS charges a late filing penalty of 5% of the unpaid tax for each month or part of a month that a return is late, up to a maximum of 25%. In addition, there is a late payment penalty of 0.5% of the unpaid tax for each month or part of a month that a payment is late, up to a maximum of 25%.

Tax Payment Options

There are several methods available for paying taxes, each with its own advantages and disadvantages. The most convenient option for many taxpayers is to pay online through the IRS website. This method is fast, secure, and allows you to make payments directly from your bank account. You can also pay by mail by sending a check or money order to the IRS. However, it is important to note that mailed payments may take several weeks to process, so it is important to allow ample time for your payment to arrive before the due date.

Payment Through a Tax Preparer

If you are not comfortable paying your taxes online or by mail, you can also hire a tax preparer to handle the process for you. Tax preparers can help you prepare your tax return and ensure that your payments are made on time. However, it is important to note that tax preparers typically charge a fee for their services, so it is important to weigh the cost of hiring a tax preparer against the convenience of having someone else handle your tax payments.

Due Dates for Tax Payments

The due date for your tax payments will vary depending on your filing status and the type of tax you are paying. In general, individual income taxes are due on April 15th. However, if you file an extension, you will have until October 15th to file your return and pay your taxes. Estimated tax payments are due on April 15th, June 15th, September 15th, and January 15th of the following year. Self-employment taxes are due on April 15th and October 15th. It is important to note that late payments may be subject to penalties and interest charges, so it is important to make your payments on time.

Explain the process of claiming a tax refund in detail, including the steps involved and the required documentation.

Claiming a tax refund involves filing a tax return and requesting a refund of any overpaid taxes. The process typically includes the following steps:

- Gather necessary documents: Collect all relevant documents, such as W-2 forms, 1099 forms, and receipts for deductions and credits.

- Choose a filing method: Determine whether to file your tax return online, by mail, or through a professional tax preparation service.

- Complete the tax return: Accurately fill out the tax return form, including your income, deductions, and credits.

- Calculate your refund: Use tax software or consult a tax professional to determine the amount of refund you are eligible for.

- File your return: Submit your completed tax return to the IRS by the filing deadline.

The required documentation may vary depending on your individual circumstances. Generally, you will need to provide proof of income, deductions, and credits claimed on your return.

Tax Audits

A tax audit is a review of an individual’s or business’s tax return by a tax authority to ensure that the information provided is accurate and that all taxes due have been paid.

Obtain direct knowledge about the efficiency of Pogacar through case studies.

The purpose of an audit is to verify the accuracy of the taxpayer’s return and to ensure compliance with tax laws. Audits can be conducted for various reasons, including:

- To verify the accuracy of deductions and credits claimed.

- To ensure that all income has been reported.

- To identify any errors or omissions in the tax return.

The audit process typically involves the following steps:

- The taxpayer receives a notice from the tax authority informing them of the audit.

- The taxpayer gathers the necessary documentation to support their tax return.

- The auditor reviews the taxpayer’s documentation and asks questions to clarify any discrepancies.

- The auditor makes a determination as to whether the taxpayer’s return is accurate.

- The taxpayer receives a notice from the tax authority informing them of the audit results.

There are several things that taxpayers can do to prepare for and respond to an audit:

- Keep accurate records of all income and expenses.

- File tax returns on time and accurately.

- Be prepared to provide documentation to support any deductions or credits claimed.

- Be cooperative with the auditor and answer all questions honestly.

- If you disagree with the auditor’s findings, you can appeal the decision.

Tax Planning

Tax planning is the process of managing your finances to reduce your tax liability and maximize your tax savings. It involves analyzing your financial situation, identifying potential tax deductions and credits, and making informed decisions about your investments and other financial transactions.

Tax planning is important because it can help you:

– Save money on taxes

– Avoid penalties and interest charges

– Protect your assets

– Plan for your financial future

There are a number of strategies you can use to reduce your tax liability, including:

– Maximizing your deductions

– Taking advantage of tax credits

– Investing in tax-advantaged accounts

– Deferring income

– Minimizing capital gains

By following these strategies, you can significantly reduce your tax liability and keep more of your hard-earned money.

Deductions

Deductions are expenses that you can subtract from your taxable income. There are two types of deductions: above-the-line deductions and below-the-line deductions.

Above-the-line deductions are deducted from your gross income before you calculate your taxable income. These deductions include:

– Medical expenses

– Student loan interest

– Alimony payments

– Retirement contributions

Below-the-line deductions are deducted from your taxable income after you have calculated your adjusted gross income. These deductions include:

– Charitable contributions

– Mortgage interest

– State and local taxes

– Gambling losses

You can only deduct expenses that are ordinary and necessary expenses for your business or investment activities. You cannot deduct personal expenses, such as the cost of your home or your car.

Tax Credits

Tax credits are dollar-for-dollar reductions in your tax liability. Unlike deductions, which reduce your taxable income, tax credits directly reduce the amount of taxes you owe.

There are many different types of tax credits available, including:

– The child tax credit

– The earned income tax credit

– The saver’s credit

– The energy tax credit

You can claim tax credits on your tax return by completing the appropriate forms.

Tax-Advantaged Accounts

Tax-advantaged accounts are investment accounts that offer tax benefits. There are two types of tax-advantaged accounts: retirement accounts and education savings accounts.

Retirement accounts allow you to save for retirement on a tax-deferred basis. This means that you do not pay taxes on your investment earnings until you withdraw the money from the account. Education savings accounts allow you to save for college on a tax-free basis. This means that you do not pay taxes on your investment earnings or on the withdrawals you make from the account.

There are a number of different retirement and education savings accounts available, including:

– 401(k) plans

– IRAs

– 529 plans

You should consider your financial situation and investment goals when choosing a tax-advantaged account.

Deferring Income

Deferring income is a strategy that allows you to reduce your tax liability in the current year by pushing income into future years. This can be done by contributing to a retirement account or by taking advantage of certain tax-deferral strategies, such as the Roth IRA.

By deferring income, you can reduce your taxable income in the current year and pay taxes on it in future years when you are in a lower tax bracket.

Minimizing Capital Gains

Capital gains are the profits you make when you sell an asset, such as a stock or a bond. Capital gains are taxed at a lower rate than ordinary income. However, if you sell an asset for a loss, you can deduct the loss from your taxable income.

There are a number of strategies you can use to minimize capital gains, including:

– Holding on to your investments for more than one year

– Selling your investments in a tax-advantaged account

– Harvesting your losses

By following these strategies, you can reduce your tax liability and maximize your tax savings.

– Discuss the various tax relief programs available to taxpayers, such as the Earned Income Tax Credit and the Child Tax Credit.

Tax relief programs are government initiatives designed to reduce the tax burden for certain groups of taxpayers. These programs can provide financial assistance to low-income families, working individuals, and parents. Some of the most common tax relief programs include the Earned Income Tax Credit (EITC), the Child Tax Credit (CTC), the Child and Dependent Care Credit, the Adoption Tax Credit, and various education credits.

Eligibility Requirements and Benefits of Tax Relief Programs

Each tax relief program has specific eligibility requirements and benefits. For example, the EITC is available to low- to moderate-income working individuals and families. The CTC is available to parents of qualifying children. The Child and Dependent Care Credit is available to parents who pay for child care or dependent care expenses. The Adoption Tax Credit is available to parents who adopt a child. Education credits are available to students who pay for qualified education expenses.

The benefits of tax relief programs can be significant. For example, the EITC can reduce a taxpayer’s tax liability by up to $6,935. The CTC can reduce a taxpayer’s tax liability by up to $2,000 per qualifying child. The Child and Dependent Care Credit can reduce a taxpayer’s tax liability by up to $1,050. The Adoption Tax Credit can reduce a taxpayer’s tax liability by up to $14,890. Education credits can reduce a taxpayer’s tax liability by up to $2,500.

Examples of How Tax Relief Programs Have Helped Taxpayers

Tax relief programs have helped millions of taxpayers save money on their taxes. For example, the EITC has helped millions of low-income families lift themselves out of poverty. The CTC has helped millions of parents provide for their children. The Child and Dependent Care Credit has helped millions of parents afford child care. The Adoption Tax Credit has helped millions of parents adopt children. Education credits have helped millions of students pay for college.

Potential Drawbacks or Limitations of Tax Relief Programs

While tax relief programs can be very beneficial, there are some potential drawbacks or limitations. For example, some tax relief programs have income limits. This means that taxpayers who earn too much money may not be eligible for the program. Additionally, some tax relief programs are phased out as taxpayers’ income increases. This means that the benefit of the program decreases as taxpayers earn more money.

Conclusion

Tax relief programs can be a valuable resource for taxpayers. These programs can help taxpayers save money on their taxes and provide financial assistance to low-income families, working individuals, and parents. However, it is important to be aware of the eligibility requirements and limitations of these programs before claiming them on your tax return.

Tax Laws and Regulations

The 2024 IRS Tables are governed by a complex set of tax laws and regulations. It is essential to stay up-to-date with these laws to ensure compliance and avoid potential penalties.

The Internal Revenue Service (IRS) is responsible for administering and enforcing the tax laws. The IRS publishes a variety of resources to help taxpayers understand their obligations, including publications, online tools, and guidance from tax professionals.

Key Tax Changes for 2024

The following table summarizes some of the key tax changes for 2024:

| Change | Description |

|---|---|

| Standard deduction | Increased for all filing statuses |

| Child tax credit | Increased to $2,000 per qualifying child |

| Earned income tax credit | Increased for all income levels |

| Capital gains tax rates | Unchanged for most taxpayers |

Resources for Staying Up-to-Date on Tax Laws

- IRS website: https://www.irs.gov/

- IRS publications: https://www.irs.gov/publications/

- Tax professionals: Certified public accountants (CPAs), enrolled agents (EAs), and tax attorneys can provide personalized advice

Failure to comply with tax laws can result in significant penalties, including fines, interest, and even imprisonment. It is important to seek professional advice if you are unsure about your tax obligations.

When investigating detailed guidance, check out Espaço Schengen now.

International Taxation

Individuals with international income or assets face unique tax implications. Understanding these implications is crucial for compliance and effective tax planning.

Foreign Earned Income Exclusion

The foreign earned income exclusion allows US citizens and residents to exclude a certain amount of foreign income from their taxable income. This exclusion is intended to provide tax relief for individuals working or living abroad.

Foreign Tax Credits

Foreign tax credits allow taxpayers to reduce their US tax liability by the amount of income taxes paid to foreign governments. This credit prevents double taxation of the same income.

Tax Treaties

Tax treaties are agreements between the US and other countries that aim to reduce double taxation and prevent tax evasion. These treaties typically include provisions on tax rates, withholding taxes, and the creditability of foreign taxes.

Offshore Banking and Investments

Offshore banking and investments can have tax implications. US citizens and residents are required to report all foreign bank accounts and investments to the IRS. Failure to do so can result in penalties.

Relevant Tax Treaties and Reporting Requirements

FATCA (Foreign Account Tax Compliance Act)

FATCA requires foreign financial institutions to report information about US account holders to the IRS. This helps prevent tax evasion and ensures compliance with US tax laws.

CRS (Common Reporting Standard)

CRS is a global standard for the automatic exchange of information between tax authorities. It helps identify and prevent tax evasion by individuals with offshore accounts and investments.

Foreign Bank Account Reporting (FBAR)

FBAR requires US citizens and residents to report foreign bank accounts with an aggregate balance of $10,000 or more at any time during the year. Failure to file FBAR can result in penalties.

Key Provisions of Major Tax Treaties

| Country | Tax Rate | Withholding Tax | Creditability of Foreign Taxes |

|---|---|---|---|

| Canada | 15% | 10% | Yes |

| France | 30% | 15% | Yes |

| Germany | 25% | 10% | Yes |

Common Tax Planning Strategies

Individuals with international income or assets may use various tax planning strategies to reduce their tax liability. These strategies include:

- Establishing foreign trusts

- Using offshore companies

- Renouncing US citizenship

Potential Legal and Financial Risks

International tax planning can carry legal and financial risks, including:

- Tax evasion

- Money laundering

- Penalties and interest

Resources for Further Research

Tax Resources

The Internal Revenue Service (IRS) offers a range of resources to assist taxpayers in understanding and fulfilling their tax obligations. These resources include:

IRS Website

- Provides comprehensive information on tax laws, regulations, forms, and publications.

- Offers online tools for tax calculations, filing, and payments.

- Contains a searchable database of tax-related questions and answers.

Tax Software

- Simplifies tax preparation by guiding users through the process step-by-step.

- Automates calculations and ensures accuracy.

- Offers features such as error checking and e-filing.

Tax Professionals

- Certified Public Accountants (CPAs), Enrolled Agents (EAs), and tax attorneys can provide expert guidance on tax matters.

- Assist with tax preparation, audits, and appeals.

- Stay up-to-date on the latest tax laws and regulations.

To access these resources effectively, taxpayers should visit the IRS website at www.irs.gov, consult with tax professionals, or utilize reputable tax software.

Key Tax Terms

Understanding the key terms used in the tax system is essential for accurate tax preparation and planning. Here are some common tax terms and their definitions:

- Adjusted Gross Income (AGI): The amount of income subject to tax after subtracting certain deductions and adjustments. AGI is used to calculate taxable income and eligibility for certain tax credits and deductions.

- Capital Gains: Profits from the sale of assets, such as stocks, bonds, or real estate. Capital gains are taxed at a lower rate than ordinary income.

- Dependent: A person who meets certain criteria and can be claimed as a deduction on your tax return. Dependents include children, spouses, and certain other relatives.

- Exemption: A specific amount of income that is not subject to tax. Personal exemptions are no longer available for the 2023 tax year and beyond.

- Filing Status: Your filing status determines your standard deduction and tax rates. Common filing statuses include single, married filing jointly, married filing separately, and head of household.

- Gross Income: All income you receive from all sources, including wages, salaries, tips, dividends, interest, and capital gains.

- Itemized Deductions: Deductions that are subtracted from your AGI to reduce your taxable income. Itemized deductions include expenses such as mortgage interest, charitable contributions, and state and local taxes.

- Standard Deduction: A specific amount that you can deduct from your AGI without itemizing your deductions. The standard deduction varies depending on your filing status.

- Taxable Income: The amount of income that is subject to tax after subtracting deductions and exemptions.

- Tax Bracket: A range of taxable income that is taxed at a specific rate. The higher your taxable income, the higher your tax bracket and the higher the percentage of your income that is taxed.

- Tax Credit: A dollar-for-dollar reduction in the amount of tax you owe. Tax credits are more valuable than deductions because they directly reduce your tax liability.

- Tax Return: The form you file with the IRS to report your income and calculate your tax liability. The most common tax return is the Form 1040.

For more information on tax terms and definitions, please visit the IRS website.

Summary

Mastering Tabelas IRS 2024 is essential for savvy taxpayers in Brazil. By leveraging the insights and strategies Artikeld in this guide, you can confidently navigate the tax filing process, optimize your tax liability, and stay compliant with the latest regulations. Embrace the power of tax knowledge and unlock the full potential of your financial well-being.